United States Office Outlook | Q2 2017 | View the Report

After a slow start to the year, the U.S. office market rebounded during the second quarter thanks to sustained tenant demand, consistent economic fundamentals and a raft of new supply. There were 11.7 million square feet of new deliveries in Q2, which helped push vacancy up to 14.8 percent. Even as demand stabilizes, asking rents for new product have risen 3.2 percent over the year and by 4.9 percent for CBD Class A space.

As for uptake of all this new space, net absorption totaled 8.8 million square feet in Q2, bringing year-to-date occupancy growth to 9.9 million square feet. 55.4 percent of that growth has come from two markets alone –Seattle-Bellevue and Dallas –powered by organic tech and corporate expansion.

While tech is still a leader in leasing volume, its share of transactions (17.4 percent) has dampened compared to previous quarters due to M&A activity and uncertainty over immigration policy.

Moving into the second half of 2017 and into 2018, we expect the wave of new supply to deliver over the next six quarters will markedly alter the office landscape, increasing competition among landlords for tenants and stabilizing rents in the process. And as tenants flock to new quality supply, we’ll continue to see slightly higher vacancy and subdued absorption of second-generation space.

1

Concession packages are rising

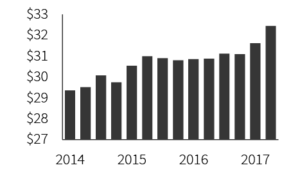

Tenant improvement allowances have jumped 10.5% since 2014, helping landlords compete for leases and tenants afford higher rents.

2

Vacancy rose slightly

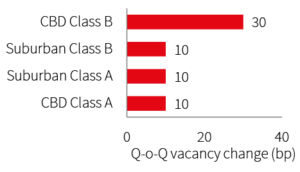

Total vacancy rose to 14.8%, with increases seen across asset classes and geographies,

particularly for Class B space.

3

Absorption is up but muted

Quarterly net absorption rose to a healthier 8.8 m.s.f., driven largely by continued

expansion in the tech sector.

By: JLL

Click here to view source article.