As we enter into the second half of 2019, we approach 10 years of recovery in the real estate markets. One question on the mind of investors is the concern over when the end of the cycle hits, one of the 2019-2020 Top Ten Issues Affecting Real Estate. While transaction volume has slowed, there is a growing disconnect between seller prices and buyer bids. One place where the market continues to be flush with liquidity is on the debt side of the capital stack. While CMBS continues to be a viable product, volume of issuance is down almost 15% year over year for the first quarter 2019 vs. 2018, and down over 12% for year end 2018 vs. 2017. Other capital markets debt products have grown in popularity and are contributing to the liquidity in the market.

Mortgage REITs is a product that has been around since inception back in 1969. While they had perception issues that impacted them in the late 1970’s, they have made a comeback over the last decade, with firms like Blackstone, TPG, ARES and Starwood creating publicly traded Mortgage REITs over the last few years. The Mortgage REITs have many financing tools at their disposal today. Part of their financing toolbox include leveraging the equity raised in the public markets with commercial real estate CLO transactions as well as securing multiple warehouse lines from investment banks and large commercial banks. Pricing, flexibility and cost will drive which financing levers are pulled.

The commercial real estate CLO market, which is a way for lenders to leverage their business, has been growing over the last few years, and is expected to continue as long as there is investor appetite for bonds. Commercial real estate CLO’s are structured finance securities collateralized primarily by below investment grade floating rate commercial real estate loans backed by bridge/transitional loans. The lender that is using the commercial real estate CLO execution, will securitize a pool of floating rate loans creating various rated bonds for investor consumption. The commercial real estate CLO issuer retains the “equity” in the commercial real estate CLO, being the most subordinate part of the structure.

The commercial real estate CLO business is a far cry from the CDO business of 12 years ago where everything and “the kitchen sink” could be put into a deal. Post crash, deals tend to be more conservative and deals tend to see senior mortgages only. Early on CRE CLO transactions were static only and like CMBS transactions needed all loans contributed in the pools by the closing. That said, CRE CLO’s still tend to have more transitional assets than CMBS whether static or not.

As the market has matured, there has been a growth of a more flexible pool, the managed pool. A managed pool differs from static in a couple of key ways. First, there is a ramp up period to add loans into the pool after the deal closes. Second, loans can be replaced in the pool. In so doing, the duration of the deals can be pushed out longer, as it is less impacted by prepayment since loans are replaced. That said, investors pay more for a static deal, not managed, because of the certainty of what the make-up of the pool is. To mitigate this concern, managed deals do have eligibility criteria to keep the quality of the pool similar to the level at closing. Managed pools are becoming more popular and the spread premium is tightening. In 2018, 54% of all deals were managed and 46% were static. In 2016 the percentages were quite different, with 25% managed and 75% static. On a year over year basis, Q1 2018 had $3.2B of issuance while Q1 2019 was at $3.6B, so the size of the market continues to grow.

Another source of significant capital in the marketplace is coming from Debt Funds, which have been established to provide both senior bridge loans as well as mezzanine loans which are secured by the equity in the borrower. The number of Debt Funds has grown exponentially over the last few years, with a universe which includes small-balance high-yield shops, and large debt funds raising capital from high net worth investors, pension funds and endowments (like Calmwater Capital) or from foreign and domestic institutional capital (like Acore Capital and Prime Finance). Time will tell if capital will shift to troubled or distressed loans in the never-ending search for yield as rough waters lie ahead.

Insurance companies like NY Life, Principal, John Handcock, MetLife and Nuveen, are leveraging their organization’s infrastructure and managing third party accounts interested in issuing debt. Even several major development firms like Silverstein, Mack Real Estate, Related Properties, S.L. Green, and Brookfield have entered the lending business. Private equity has its role in the marketplace as well, with Blackstone, Colony, Oaktree, INVESCO, CIM and Starwood providing liquidity to the market, particularly on larger deals. Investment Banks and Commercial Banks like Morgan Stanley, Citigroup, JP Morgan, Wells Fargo and Bank of America are wearing multiple hats, originating loans, providing leverage via warehouse lines, or managing the execution of CLO’s. In fact, the Commercial Banks use their ability to provide warehouse lines to garner the CLO business from their borrower clients! Whether a borrower needs a $2M, $20M or $200M loan, there are multiple options for the debt.

When we look at the composition of lenders in the market, CMBS, Debt Funds and REIT’s represented 26% of total issuance in both 2017 and 2018. Within that segment, we did see a shift from CMBS to Debt Funds and REITs, with CMBS at 19% of the 26% in 2017 and 16% of the total in 2018. Liquidity from Funds and REITs are providing alternatives, and with the debt markets flush with liquidity and competition for transactions fierce, the question to ask is whether we are headed for rough waters with the possibility of credit and structural deterioration.

By: Constantine Korologos, CRE®, MAI, MRICS and Jeffrey Lavine, Esq (CRE)

Click here to view source article

Sales

Total sales volume in 2019 Q3 rose at a modest pace of 3% from a year ago. Sales growth has moderated since 2017 compared to the almost 10 percent growth per year since 2012 through 2016.

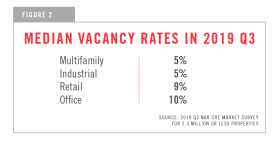

By asset class, respondents reported strong sales in apartment and industrial markets. The median going-in cap rates for all property types was 6.6%, with apartment properties having the lowest median cap rate, at 5.9%, followed by industrial warehouse, at 6.5%. Retail strip centers had the highest cap rate, at 7.1%. Cap rates continue to decline, especially for apartments and industrial properties given the demand for these types of properties (falling cap rates = rising prices).