Introduction

Seniors housing properties have begun to recover from the deep impacts COVID-19 had on the sector in 2020.

The seniors housing sector is continuing to deal with the lingering effects from the COVID-19 pandemic, including lower occupancies and higher expenses, which are squeezing net operating incomes and weighing on transaction activity. Yet the 2021 WMRE / NIC Seniors Housing Survey shows growing confidence in the sector’s outlook, including improving fundamentals and a rise in investment activity over the next 12 months.

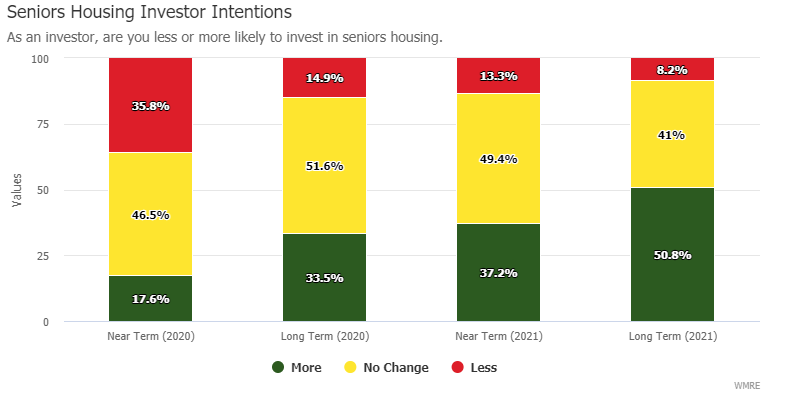

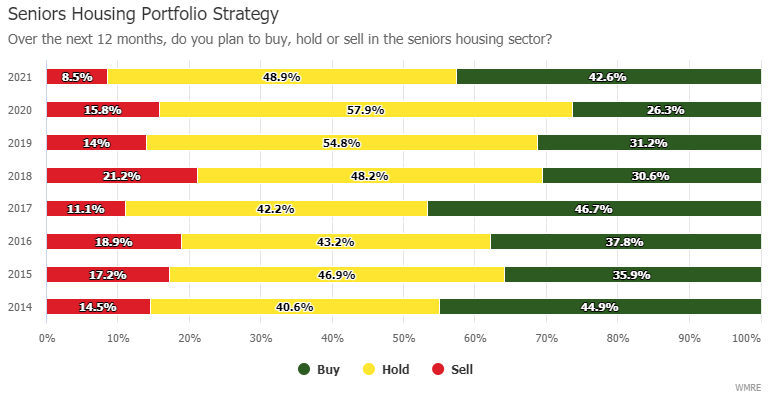

Capital that moved to the sidelines last year is preparing to get back on the playing field. In all, more than one-third of survey respondents said they plan to invest in seniors housing in the near term—double the 18 percent who planned near-term investments in the 2020 survey, which was conducted in the midst of the pandemic. Investors are even more bullish on their long-term investment plans. About half (51 percent) expect to invest more in seniors housing assets over the long-term, which is up from 34 percent a year ago.

“Part of that rebound is due to the underlying demographic characteristics, but the value proposition is still there,” says NIC Chief Economist Beth Burnham Mace. From an investor’s point of view, seniors housing diversifies portfolios, often performs counter-cyclical to the economy and has a track record of delivering favorable long-term returns. According to the NCREIF Property Index (NPI), seniors housing generated an 11.5 percent annualized total investment return for the 10-year period ending in first quarter of 2021. That compares favorably to the overall return of 8.8 percent for the NPI. “The appeal of seniors housing is still very much driven by the demographics story, and that story has brought in a lot of capital,” says Mace. The leading edge of baby boomers born between 1946 and 1964 are 75 today, whereas the average age that someone enters a seniors housing care facility is 82. So, the wave of demand is still several years away, but it is getting closer every day, she adds.

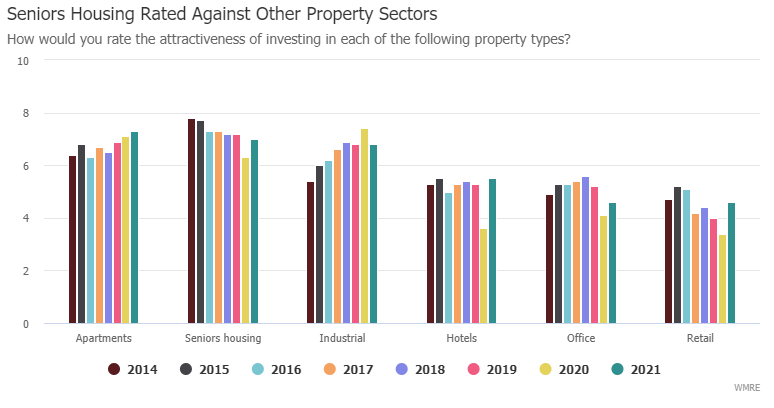

Despite challenges that have hindered the sector over the past year, respondents continue to view seniors housing favorably compared to other property types. On a scale of 1 to 10, seniors housing generated a mean score of 7.0, which was second only to apartments at 7.3 and even slightly ahead of industrial at 6.8. Although the current rating is an improvement from the 6.3 rating that seniors housing had in the 2020 survey, it still represents the second lowest level in the eight-year history of the survey.

“COVID has been extremely challenging for the senior housing industry given residents are highly vulnerable. That being said, the industry seems to have hit bottom early in ’21 and occupancy has been building since then,” says Lukas Hartwich, a managing director at Green Street Advisors. “The biggest tailwind for the industry continues to be the nascent demographic wave of seniors, which is just around the corner, while the biggest headwind will likely continue to be supply growth and labor cost pressure,” adds Hartwich.

Survey methodology: The WMRE /NIC research report on the seniors housing sector was conducted via an online survey distributed to WMRE readers in June. The 2021 survey results are based on responses from 189 participants. The majority of respondents hold top positions at their firms with 50 percent who said they were either an owner or C-suite executive. Respondents also represent a cross-section of different roles in the seniors housing sector, including investors, lenders, developers, brokers and owner/operators.

Buyers Return to Market

Investment sales activity has picked up for seniors housing properties.

The pace of investment sales in 2021 is below pre-pandemic levels. According to Real Capital Analytics, seniors housing single asset, portfolio and entity level deals totaled $5.8 billion through May. Although that is on par with 2018 sales for the same period, it is about 21 percent behind the 2019 pace.

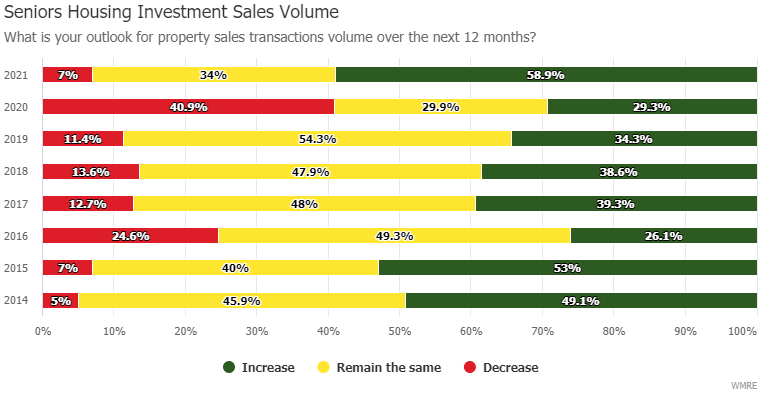

Respondents are more confident that transaction will accelerate over the next 12 months. A majority 59 percent think transaction volume will increase compared to 29 percent who held that view in the 2020 survey.

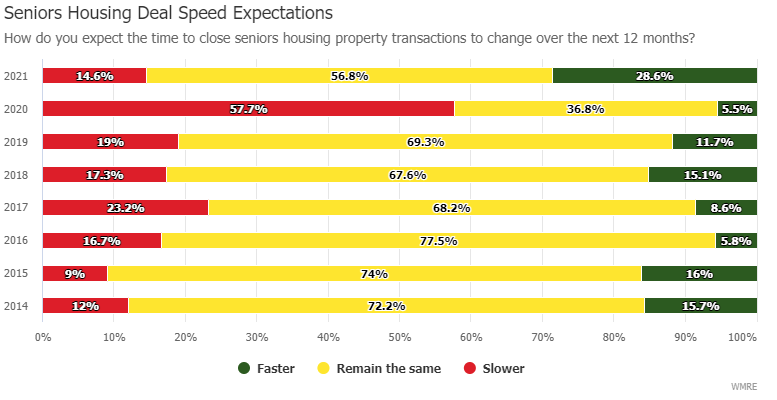

When asked about the change in time to close transactions, 57 percent expect it to remain the same over the next 12 months, while 29 percent said it could be faster and 15 percent anticipate slower closings.

“We know that the baby boomers are coming. The vaccine is in place; construction is down; and replacement costs are way up, and pent up demand is there,” says Mark Myers, managing director, investment sales at Walker & Dunlop. “At the same time, you have very inexpensive capital, and many buyers and sellers are still there waiting on the sidelines. As buyers reenter the space, demand will increase, pricing will increase, and this bodes well for very positive transaction activity over the next few quarters.”

In fact, investment sales have picked up significantly in the past two months with REITs leading that charge. Ventas announced in June that it was acquiring New Senior Invest Group in a deal valued at $2.3 billion. Welltower Inc. is acquiring a portfolio of 86 independent living (IL) and assisted living (AL) properties owned by Holiday Retirement for $1.58 billion. Another sign of the increasingly positive investment climate is that Bridge Investment Group, which has a seniors housing portfolio valued at roughly $4.5 billion, filed for an IPO in June.

Healthcare REITs are becoming more active on the external growth front both in terms of acquisitions and development. In addition to the recent wave of announcements, management teams are communicating that there is more to come, notes Hartwich. There are many factors that are driving the increase in REIT transaction activity. Part of the answer is that there are more willing sellers than there were in 2020. “Perhaps the biggest driver is the cost-of-capital advantage that many health care REITs enjoy,” he says. Several health care REITs have the ability to buy assets in the private market for 100 cents on the dollar with capital that is priced more richly, in some cases in excess of 125 cents on the dollar, he adds.

Outside of the REITs, sales activity has been slower to return. “What is holding things up is that COVID did have a dampening effect on occupancy,” says Myers. Some operators closed their doors for 12 months or more to protect their most vulnerable residents. Falling occupancy levels squeezes profit margins, which in turn impacts underwriting and pricing. Owners are more likely to hold assets that don’t have stabilized occupancies rather than sell at a discount.

“People aren’t going to wait for a full recovery to start going after buying opportunities. They’ve already started to do that,” says Myers. Pent-up demand following the Great Financial Crisis was like a switch turning on that saw a surge in commercial real estate in 2010 and beyond. “I think you’re going to see a similar thing happen here once properties regain occupancies, probably starting at the end of third quarter and beginning of fourth quarter,” he says.

The Sector Shifts to Recovery Mode

Respondents are bullish that fundamentals will improve over the next 12 months.

Twelve months ago, the outlook for seniors housing was decidedly bleaker. More than half of respondents in the 2020 survey considered seniors housing to be in a recession or a trough, while another one-fourth were not even sure of the cycle. Half of respondents (51 percent) now see the seniors housing sector in the recovery/expansion phase compared to 20 percent who think it is in a recession/trough, 18 percent who are unsure and 12 percent who believe it could be at the peak.

Naturally, there are questions about how quickly the seniors housing market will recover, and what that path of recovery will look like, notes Mace. “Until we see that inflection point where we start to see strong improvement, the low overall occupancy rates are still a significant concern in how quickly the market comes back,” she says.

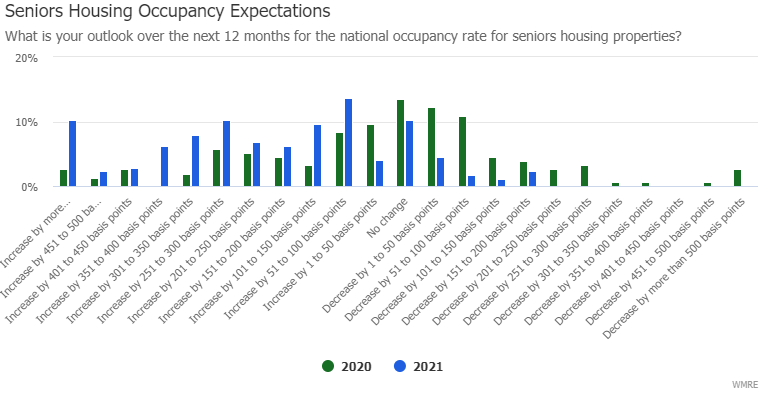

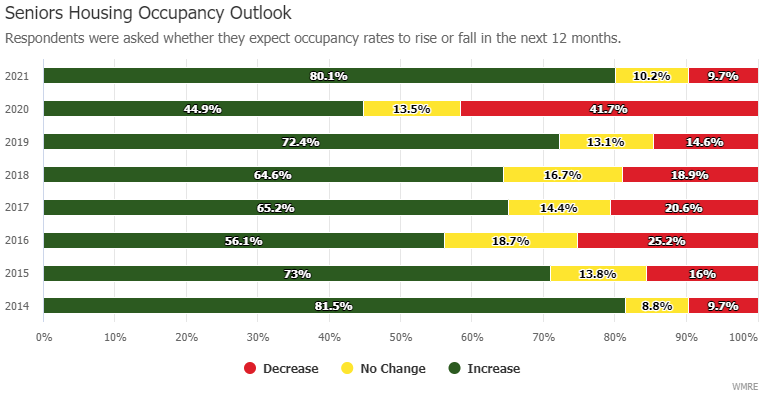

Survey results do show a surge in optimism for improving occupancies over the next 12 months. Eighty percent of respondents expect occupancies to rise. That is a big jump compared to the 45 percent who thought occupancies would rise in the 2020 survey.

According to NIC MAP data, powered by NIC MAP Vision, senior housing occupancy in the United States remained flat in second quarter at a record low of 78.8 percent. AL and IL properties both experienced little change in occupancy, with IL holding steady at 81.8 percent and assisted living inching up to 75.5 percent. However, there was positive quarterly absorption that was offset by new supply.

A deeper look at the NIC MAP data shows that a growing number of operators are reporting occupancy increases. In the second quarter of 2021, 47 percent of senior housing properties in the NIC MAP Primary Markets reported an increase in occupancy. During the height of the pandemic, that number was 22.5 percent. “We have anecdotes of improvement, but it hasn’t shown up yet in the data through second quarter. So, it is understandable that investors are approaching the sector with caution,” says Mace.

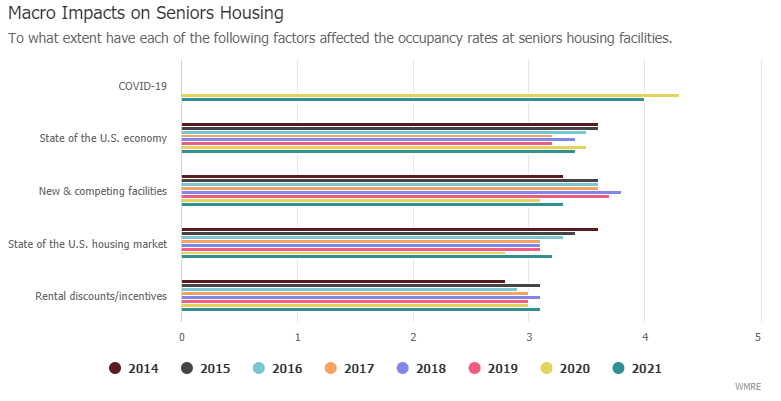

Despite high vaccination levels among senior housing residents, COVID-19 continues to have a significant impact on occupancy rates at seniors housing facilities. On a scale of 1 to 5 with 5 representing a significant impact, respondents rated COVID-19 as the biggest factor impacting occupancies at 4.0. That does show an improvement over the 4.3 in the 2020 survey.

It is likely that strength in the economy and hot housing market are providing a positive counterbalance to the negative leasing effects caused by COVID-19. In fact, the 3.2 rating on the housing market increased from 2.8 in 2020 and is also up slightly from the 3.1 rating from the prior three years.

Some seniors are taking advantage of the hot housing market to sell their home at potentially peak pricing and shift to rental housing. According to the National Association of Realtors, the median existing-home price for all housing types saw a record year-over-year increase of 23.6 percent in May with homes selling after an average of 17 days on the market.

Greater Expenses Squeeze Profits

COVID-19 has boosted operational expenditures and many operators expect those higher costs to persist.

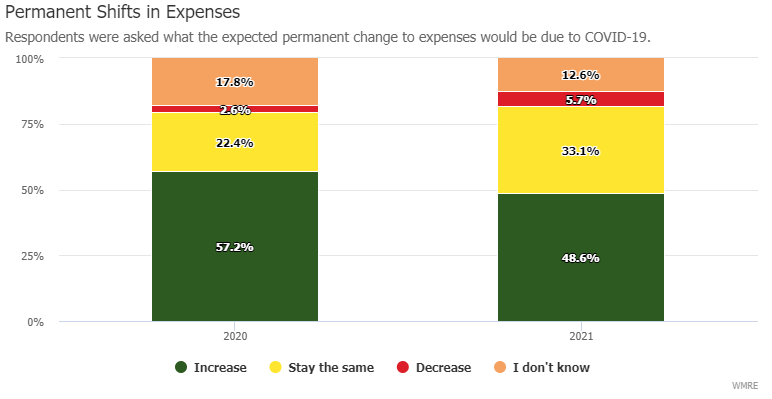

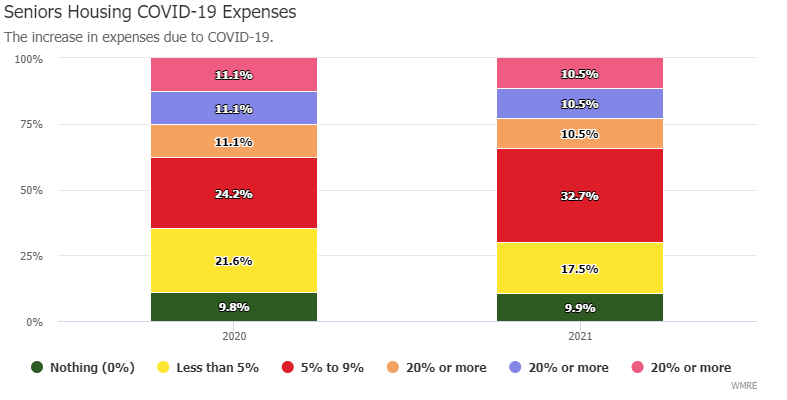

As operators work to regain leasing momentum, they face the added challenge of higher operating expenses. Consistent with the 2020 survey results, the vast majority of respondents (90 percent) saw an increase in their expenses with an estimated mean increase of 9.1 percent. Nearly half of respondents (49 percent) believe those COVID-19 related increases are likely to be permanent. It is notable that the percentage that hold that view has improved compared to 57 percent in the 2020 survey who expected the increased expenses to be permanent. One-third of current survey responds think that expenses are more likely to normalize, 6 percent believe expenses could decline and 13 percent remain unsure.

“Expense pressure is here to stay, and it’s stemming from a few places,” says Mace. Foremost, is labor. Data from the BLS on Average Hourly Earnings for AL properties, for example, were up 5.4 percent at year-end 2020 on a YOY basis. However, hourly earnings also were trending higher before the pandemic. A number of states have increased their minimum hourly wage rates, while difficulty in finding workers and reliance on higher cost temporary workers also are contributing to higher labor costs. Salary and labor expenses are about 60 percent of an operator’s expense load. On top of that is extreme pressure on expenses from insurance rates that are going up across the board as a consequence of the pandemic. There also are likely to be permanent changes associated with the pandemic, such as more focus on cleaning, sanitizing and maintaining a supply of PPE for preparedness of an infectious outbreak.

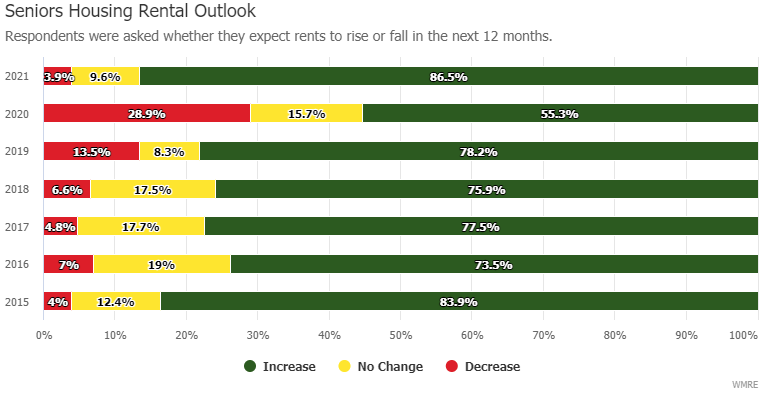

On a positive note, survey respondents are more optimistic on rent growth ahead. A majority of respondents (87 percent) expect an increase in rents over the next 12 months with an average increase of 261 basis points. That is a big shift compared to the 54 percent who thought rents were likely to rise a year ago, and it is more bullish than previous surveys where upwards pf 70 percent of respondents over the prior five years were confident that rents would continue to rise. According to NIC MAP data, asking rents grew by 1.2 percent in second quarter.

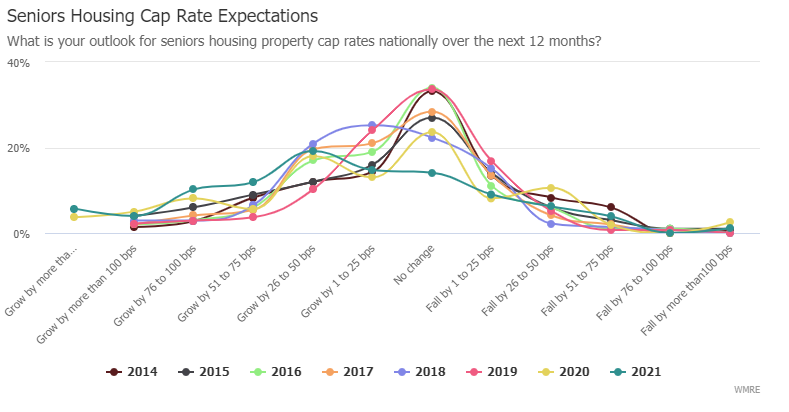

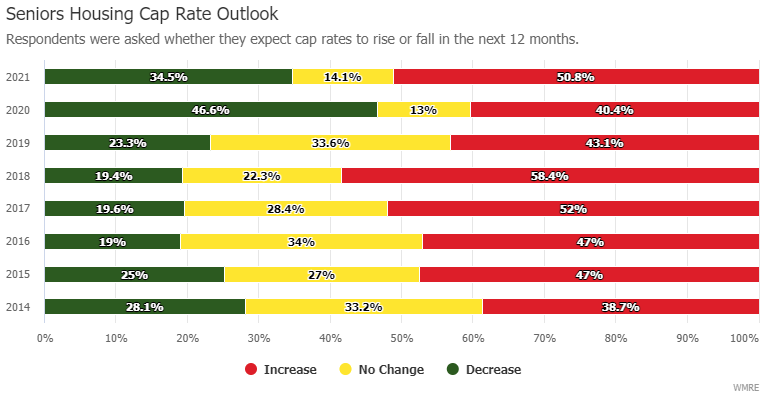

Pressure on NOI is making buyers understandably more cautious on cap rates they are willing to pay for assets. Two-thirds of investors expect cap rates to rise over the next 12 months. That shows a noticeable uptick compared to both 2020 and 2019 survey results where 53 percent and 43 percent respectively thought cap rates would increase in the coming year.

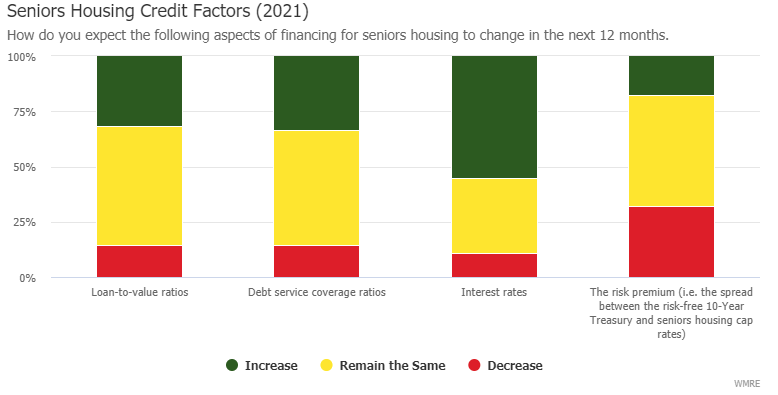

The outlook for higher cap rates is likely tied to anticipation of higher interest rates ahead. Nearly two-thirds of investors believe interest rates will increase over the next 12 months compared to 30 percent who said there will be no change and 5 percent who predict a decline. Additionally, 48 percent think the risk premium will rise, 40 percent anticipate no change and 13 percent believe the risk premium could decline.

Construction in the Sector Slows

Respondents do expect the pace of building to increase in the next 12 months.

A slowdown in construction and a reduced amount of new supply coming on to the market should help speed the recovery. Construction starts fell sharply after the start of the pandemic in second quarter 2020 and that more subdued pace has continued into second quarter 2021. According to NIC MAP data, construction as a percentage of inventory was 5.0 percent in first quarter, which has declined from levels of 6.6 percent prior to the pandemic in first quarter 2020.

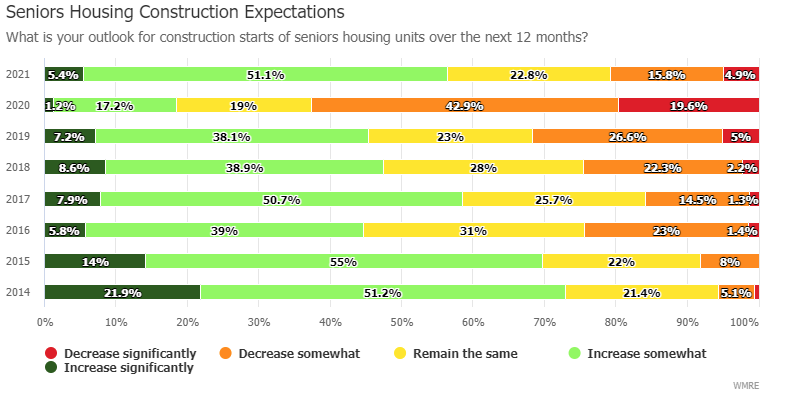

However, respondents expect to see construction pick-up. Fifty-six percent of respondents anticipate seniors housing construction starts to increase over the next 12 months compared to just 18 percent who predicted an increase in the 2020 survey. Nearly one in four respondents believe construction starts will remain the same in the coming year, while 21 percent think construction could decline.

Minneapolis-based Ryan Companies US Inc. is one developer that powered through the pandemic and sees more opportunities ahead. The firm typically averages five project starts per year, and the number of projects it kicked off during 2020 increased to seven. “There was a good opportunity for us to move forward with projects that, when they open two years from now, will have less competition pressure than we’ve had in the last five years,” says Julie Ferguson, senior vice president and sector leader, Senior Living at Ryan Companies US Inc.

Ryan Companies builds communities with a combination of IL, AL and memory care. Its current pipeline of active and planned projects spans 22 senior living developments totaling 4,000 units and valued at more than $1.5 billion in total project costs. Ferguson is not concerned about oversupply in markets that the company has targeted for growth, which include California, Florida, Illinois, Minnesota, Tennessee, Texas, Washington and Wisconsin. “We do heavy due diligence on where we locate communities, as do our peers as we are a very data driven industry,” says Ferguson. “So, while there is a lot of competition, we all look at things slightly differently.”

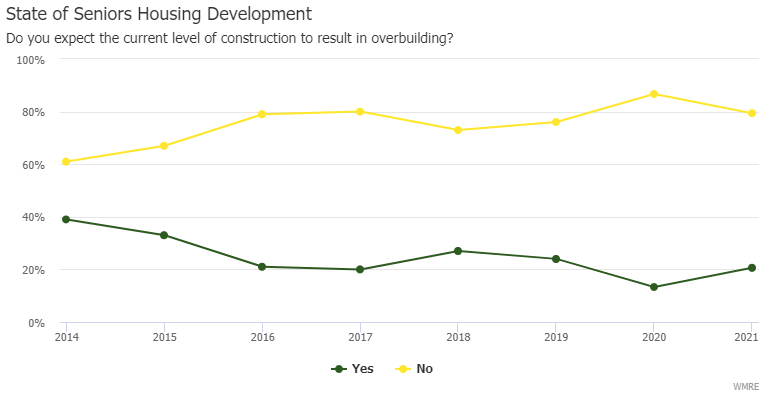

A majority of survey respondents (79 percent) do not think new construction will result in overbuilding. Although it represents a strong majority, sentiment has pulled back from a high of 87 percent in the 2020 survey who were not concerned about overbuilding. Higher construction costs could make it more difficult for some new projects to move forward, especially when also accounting for higher operating costs.

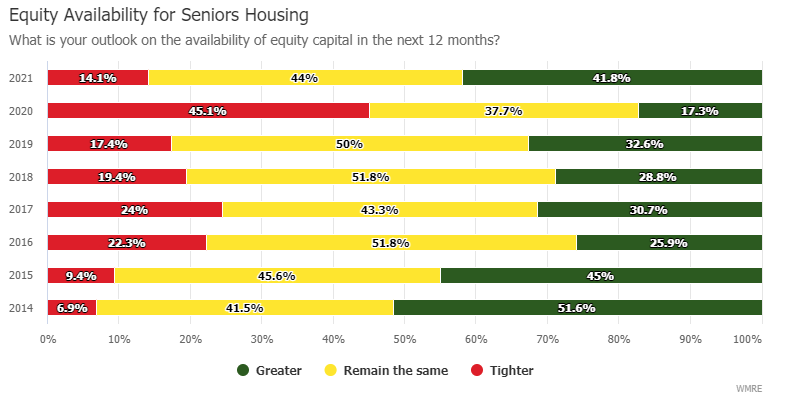

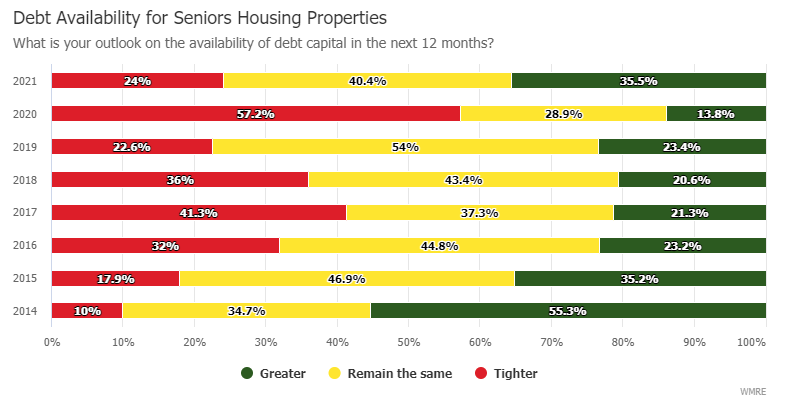

Capital Moves Off the Sidelines

Industry pros expect debt and equity to become more available in the next 12 months.

Money is starting to come back to the seniors housing sector after a near total shut-down in financing for new deals during the pandmic. Respondents expect the availability of both debt and equity to improve over the next 12 months. Although 44 percent think availability of equity will remain the same, 42 percent believe it will increase and only 14 percent anticipate a decline. That outlook is distinctly more favorable compared to the 2020 survey where 45 percent predicted that it would be more difficult to access equity.

On the debt side, 40 percent believe there will be no change, while 36 percent said availability is likely to increase and 24 percent predict a decline. That sentiment also shows a marked improvement to 2020 when 57 percent thought availability of debt would be tighter.

“The liquidity in the capital markets right now is tremendous,” says Myers. Unlike the 2008 crisis, capital sources during the pandemic were not put at risk. So, when the vaccine came out and the public health crisis began to recede, those various capital sources remain well positioned. Banks, for example, are sitting on billions (if not trillions) in liquidity due to increased deposits from stimulus money. In addition, some of the mortgage REITs are borrowing at 77 basis points over LIBOR, notes Myers. “What you’re seeing is low cost of capital that is prompting investors to say, ‘let’s get something done, because there may never be a time when capital is this affordable again,” he says.

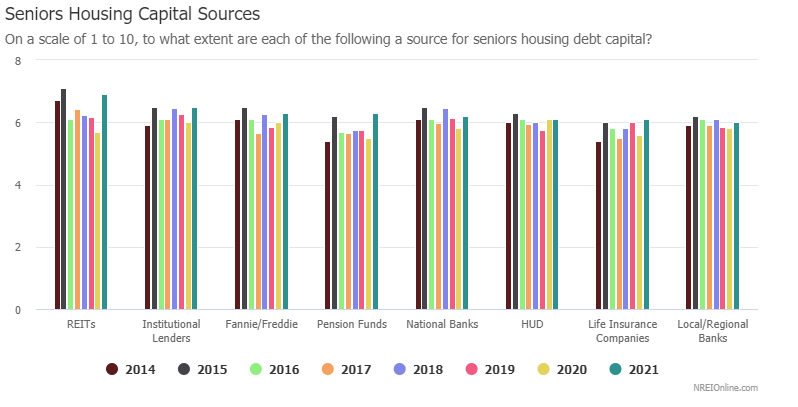

Although banks have traditionally been viewed as a top source of capital in prior surveys, the 2021 survey shows that REITs are now viewed as the most significant source by 42 percent of respondents followed by institutional lenders at 34 percent, pension funds at 32 percent and Fannie Mae/Freddie Mac at 31 percent. Banks rated lower in the survey with local/regional banks at 28 percent and national banks trailing at 24 percent.

That shift in sentiment could be a reflection of the “spottiness” in the bank financing market right now. Some banks have a lot of seniors housing loans on the books that were impacted by the pandemic that may have debt service coverage ratios (DSCRs) below 1.0x. Banks that have that exposure are not going to be willing to put a lot more capital into the market until occupancies improve, notes Stephanie Anderson, head of seniors housing and healthcare at Berkadia. Those banks that have less on their balance sheets are willing to do recourse loans at 1.0x DSCR in anticipation of lease-up ahead. However, anything below 1.0x DSCR is very difficult to achieve in the current market, she adds. According to Anderson, REITs also could be in favor because they are willing to provide higher leverage—up to 90 percent LTV.

Half of respondents predict no change to underwriting over the next 12 months, while 32 percent expect underwriting to become tighter and 18 percent who said standards are more likely to loosen. Although more than half of respondents expect no change to DSCRs and LTVs, 34 percent do think that DSCRs could increase, and 32 percent believe LTVs could increase.

There is a lot of equity capital, as well as a lot of B-piece mezzanine capital, on the sidelines waiting for more stabilization and “underwritable” deals. Investors are cautiously getting off the sidelines and those deals are coming out to the market for financing, notes Anderson. “Historically, seniors housing has been seasonal with more occupancy gains in third quarter. So, we’re coming up to a real test,” she says. Lenders will be watching those numbers closely to see if it will be a long road back or a quicker recovery. “If there is a lot of contraction in vacancy in third quarter, then I would expect that we will see everyone diving back in and loosening underwriting standards,” she adds.

Source: “Cautious Optimism Returns to Seniors Housing Market”