Real estate is an integral part of economic activity, with transactions providing avenues for exchange, development, and growth opportunities. Within this framework, like-kind exchanges (LKE) provide an important vehicle to sell and acquire property. The Internal Revenue Code (IRC) Section 1031 codifies that the tax owed on any gain after a sale may be deferred as long as the proceeds are reinvested in a similar property through a like-kind exchange. The Internal Revenue Service (IRS) makes note of the fact that while the gain “is tax-deferred […] it is not tax-free.”[1]

Like-kind exchanges are available to individuals, partnerships, corporations, limited liability companies, as well as trusts. The main requirement of a like-kind exchange is that the sale of one property and acquisition of another property must be part of an integrated transaction, rather than two individual transactions. In addition, while both real and personal property qualify, the properties must be similar, pursuant to specific criteria which delineate eligibility.

According to the IRS, “like kind property is property of the same nature, character or class. […] Most real estate will be like-kind to other real estate.”[2] Generally, a parcel of land with a rental house may be exchanged for vacant land. Similarly, an office building may be exchanged for an industrial warehouse or a retail shopping center.

Like-kind exchanges (LKE) feature prominently in NAR members’ real estate transactions, as well as their clients. As most REALTORS are small business owners, and as they represent through their clients a wide swath of small businesses across the country, LKE transactions reflect both the diversity and character of Main Street.

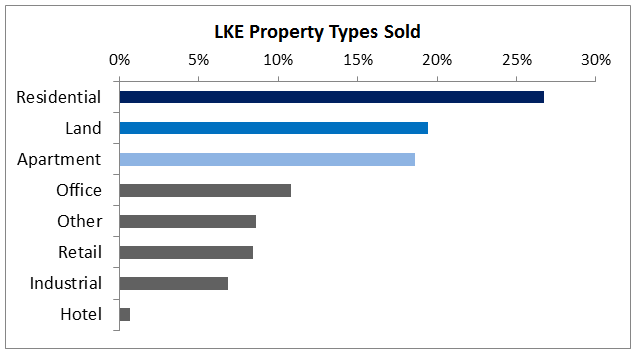

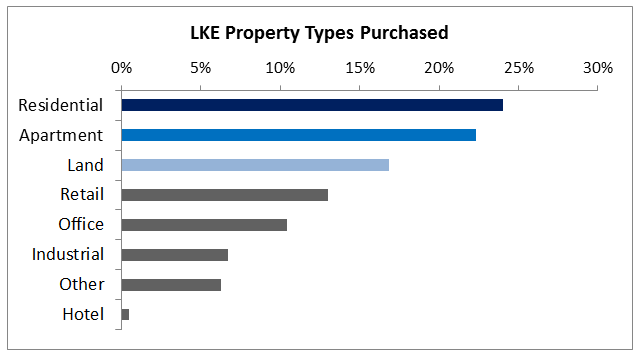

The Like-Kind Exchanges: Real Estate Market Perspectives 2015 report illustrates the full property spectrum which touches every facet of the American economy. Based on REALTORS® responses, residential properties comprised the largest proportion of recent deals, accounting for 27 percent of disposed properties and 24 percent of purchased properties, respectively. Apartments accounted for about one-in-five sale transactions, and 22 percent of acquisitions. Apartments ranked third in disposals and second in purchases, trading ranking spots with land.

Land assets accounted for 19 percent of disposals and 17 percent of acquisitions. Retail properties accounted for 13 percent of acquisitions and 8 percent of disposals. Office buildings comprised 11 percent of properties disposed and 10 percent of properties acquired. Industrial buildings made up 7 percent of both total disposals and acquisitions. Hotel transactions were a minor share of all transactions.

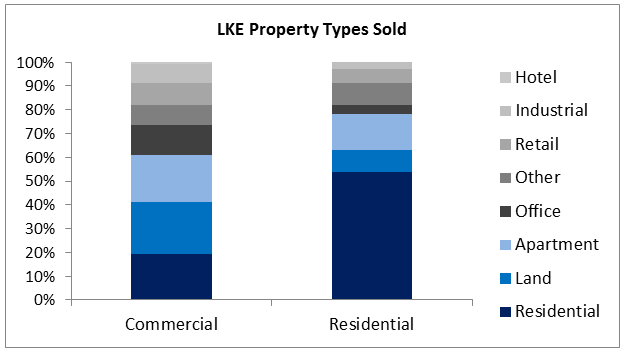

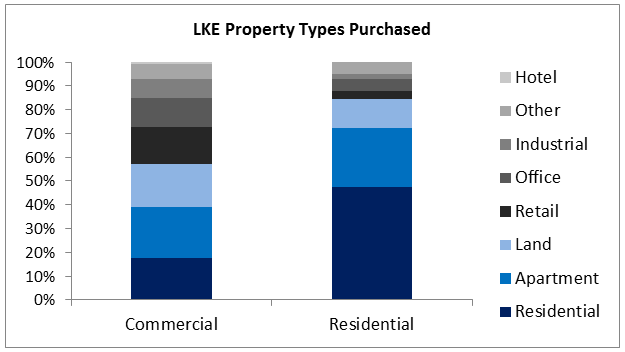

Properties disposed and purchased through like-kind exchanges mirrored NAR members’ practice specialty areas. Residential members handled a significantly larger share of residential properties, which comprised 54 percent of dispositions and 48 percent of acquisitions. Residential members also participated in a noticeable share of apartment transactions, accounting for 15 percent of dispositions and 25 percent of acquisitions. Conversely, commercial members were more active across the commercial property types—office, land, retail, apartment and industrial.

To access the Like-Kind Exchanges: Real Estate Market Perspectives 2015 report, visithttp://www.realtor.org/reports/like-kind-exchange-survey.

By: George Ratiu and Erin Fitzpatrick (Economists’ Outlook)

Click here to view source article.

Commercial Association of REALTORS® - CARNM New Mexico

Like-Kind Exchanges – Integral to Residential and Commercial Real Estate Transactions

07.15.2015

{kind=link}

© 2024, Content: © 2021 Commercial Association of REALTORS® New Mexico. All rights reserved. Website by CARRISTO