Financing conditions tighten as lenders face more-stringent regulations.

While commercial real estate is coming off a great year for transaction volume and pricing in 2015, it’s been a difficult first quarter for the economy, and suddenly projections for commercial real estate’s performance this year are being revised downward, according to many market sources. Is it going to be difficult for borrowers to find financing for CRE projects this year? CIRE surveyed lenders in various U.S. markets to get an overview of today’s lending trends.

Participants

Shahid K. Abdulla, CCIM; senior vice president/commercial lender; PlainsCapital Bank, San Antonio, Texas

Tricia Callies, CCIM, Rainmaker Lending Capital, LLC/director, KW Commercial, Boise, Idaho

Ed Craine, CCIM, CEO, Smith-Craine Real Estate Financing, San Francisco

Maryann Mize, CCIM, senior vice president/senior credit officer, Charlotte State Bank & Trust, Port Charlotte, Fla.

Is commercial real estate in a bubble right now? Are prices too high in terms of fundamentals? What is your view given your market?

Maryann Mize, CCIM: Generally speaking, Southwest Florida is not in a bubble, and in fact there are still great opportunities.

Shahid K. Abdulla, CCIM: I do not believe that there is a commercial real estate bubble in the current economy. However, we are pushing the envelope on single tenant triple net lease investments and multifamily assets. Capitalization rates are hovering in the mid-4 percent to mid-6 percent, which may or may not adequately price the risk inherent with the subject asset. For example, a Chick-Fil-A or Chase Bank NNN investment will trade in the 4 to 5 percent cap rate, but they are special purpose buildings, which would or should have a risk adjustment on pricing if they go dark. However, a significant amount of liquidity is in the marketplace looking for perceived safe haven investments, so pricing has been adjusted accordingly. Many of these assets do not underwrite for debt and require an all-cash purchase.

With regard to multifamily, many developers build to a 6.5 percent cap rate, versus build to an 8 percent cap rate and transact in the mid-6 percent. This does not build enough risk into the projects for any market adjustments. Additionally, all new multifamily development only project rents upward based on the most recent transaction, with little regard for concessions or vacancy. Most if not all new projects rely heavily on high occupancy and other income (garages or views) with per square foot rents at or near the peak.

Tricia Callies, CCIM: I do not think commercial real estate is in a bubble in the Boise area. Cap rates are pushing downward as evidenced by sales prices and appraisals. Our market is strong, growing, and we can expect good things for several years to come. That is not just my being an optimist. Boise is estimated to grow by 185,000 by 2020.

Ed Craine, CCIM: While I wouldn’t say we’re in a bubble, there is a great concern that we’re approaching the end of this cycle and that prices will inevitably correct. For example, builders I work with are not currently purchasing land that they can’t immediately develop and build on. They believe that in the next two to three years we could be in a downturn. Long-term investors I work with have been moving to and increasing their cash positions in anticipation of buying opportunities. My view is that we have another year or two of steady and possibly slightly increasing prices for most asset types, but that in the next few years an event or series of events could trigger a crisis in confidence that will lead to a market correction.

What is the effect of new banking regulations on loans in your area?

Mize: As a banker with more than 35 years of experience, I can’t recall a time when the banking industry hasn’t had to adapt to changing regulations. The current wave of changes impacts the way we do business internally, but in my opinion, doesn’t impact the borrower.

Callies: My lending sources are not dependent on local banks; however I have found our local banks eager to lend regardless of new regulations. They are just making adjustments to the new rules.

Craine: Every banker I work with has this same problem: regulators in their shops all the time, constantly asking them to justify their credit decisions. Oversight is at unprecedented levels. This leads to more cautious underwriting, greater requests for documentation, and more conservative lending.

Abdulla: The continued regulatory burden is causing banks to add resources in their risk management areas. This impacts the bottom line for smaller banks, more so in rural communities that do not see the level of loan demand as in growing metro areas. The consideration for Basel II and high volatility commercial real estate are keeping some larger lenders from pursuing good loan opportunities for fear of exceeding regulators’ guidelines for construction and commercial real estate loan commitments.

How have underwriting standards changed in the past couple of years?

Callies: They have gotten tougher; it was needed.

Abdulla: Over the last 12 to 18 months we have seen many new lenders with loose underwriting standards enter our market. They have been offering non-recourse construction loans and higher loan to value’s with little to no loan covenants. It becomes challenging to compete as borrowers begin to think that this is the norm.

Craine: Borrower quality rating is more important and more scrutinized than ever. Sensitivity to BQR scores is higher than ever. This is especially true for owner/user properties. Zoning and compliance issues are reviewed and scrutinized in much greater detail than in the past. Lender inspections for health and safety issues as well as physical condition have taken on increased importance and attention.

Mize: If we are comparing where we were in 2007, yes, things have changed, and probably needed to change in light of the frothy lending that was going on that subsequently resulted in losses to both banks and investors.

What is the effect of crowdfunding or other forms of competition on your institution’s ability to find and fund good deals?

Mize: None that I am aware of at this time in our small, sub-tertiary market. I certainly would be interested in any studies done on this topic, especially as it relates to Main Street America.

Callies: I have not done a crowdfunding deal; however I know a few who have sought funding through this source and found the experience a good one.

Craine: This hasn’t affected my business yet, but I’m watching carefully. It could be a great source of funds for my clients.

Abdulla: The level of crowdfunding has increased to where we are seeing a lot of private lending at or near market rates. In the past, the only private lending was from hard money lenders, well above any market rates, and typically for projects that would not underwrite in a traditional bank environment. Thus, there is a level of business that is not getting closed with the traditional commercial banks.

What is the biggest challenge commercial real estate borrowers face for the remainder of the year?

Mize: Making a decision. As an investor, is it a good decision to buy based on what part of the real estate cycle in the given market and product? For an owner/user, if they are renting, is now a good time to buy? The reality is that there are a lot of favorable fundamentals in play, including low-interest rates.

Callies: Probably time. I don’t think that the owners who need to refinance in 2016 and 2017 understand the urgency to start the process as soon as possible.

Craine: Biggest challenges are finding suitable local property at any price and finding local property at a “fair” price – one that works for the buyer. And there is loan pricing uncertainty going into higher leveraged deals due to pricing adjustments arising from loan to value, discounted cash flow, global cash flow requirements, and other risk factors that can impact final pricing.

Survey Says

In March, the National Association of Realtors surveyed commercial Realtors to determine current commercial lending trends. The biggest surprise from this year’s survey? The increase in the number of Realtors reporting a tightening of lending conditions, says George Ratiu, NAR’s director of quantitative and commercial research, who conducted the survey and analyzed the results. This year, 33 percent of members surveyed said lending conditions have significantly or somewhat tightened in the past 12 months. That compares with only 22 percent in 2015 who made the same observations. Read complete survey results at www.realtor.org/reports/commercial-lending-trends-survey.

Survey Highlights

• 61% of respondents closed sale transactions in 2015

• Realtors closed an average of 8 commercial sales

• 94% of sales were valued below $5 million

• Cash comprised 26% of all transactions

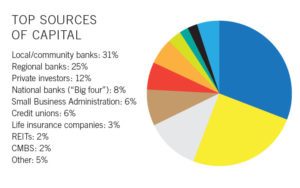

• 61% of transactions had financing with loan to value equal to or higher than 70%

• Debt-to-service coverage ratio was 1.4.

• 27% used the Small Business Administration refinance program

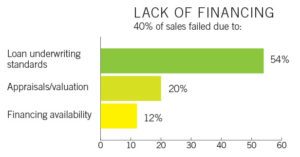

• 15% of deals failed to secure refinancing, compared with 50% in 2012

By: Sara Drummond (CCIM Institute)

Click here to view source article.