The Mortgage Bankers Association anticipates a slight decline in velocity for multifamily originations in 2018.

“Commercial and multifamily markets remain strong, even as many growth measures are exhibiting a bit of a downshift,” says MBA’s Woodwell.

Two mortgage banking sectors, one organization, one slow-growth economy, two divergent outlooks for the coming year. The Mortgage Bankers Association said last week that it expects commercial and multifamily originations to be essentially flat in 2018. On the residential side, though, MBA is expecting a year-over-year increase in purchase mortgage originations, even as refinancing activity is expected to slide.

Flat growth doesn’t equate to a decline in volume, though. MBA’s latest prediction of a 5% annual increase in commercial and multifamily originations this year, to $515 billion, comes after the association’s projection in June of a slight decline for 2017 volume.

Yet if the prediction holds true that next year will show essentially no gains over ’17 levels, it will represent the first year since 2009 that Y-O-Y comparisons for commercial and multifamily mortgages don’t represent a meaningful increase. The annual growth rate was steeper in the years following the Global Financial Crisis—2010 volume was 44.8% over the year prior, for example, and 2011 brought another 55% improvement—but each year since the downturn has seen larger numbers than the one before.

“Commercial and multifamily markets remain strong, even as many growth measures are exhibiting a bit of a downshift,” says Jamie Woodwell, VP of commercial real estate research. “Property values are up 6% through the first eight months of this year.

“Despite a decline in property sales transactions, commercial and multifamily mortgage originations were 15% higher during the first half of this year than a year earlier,” he continues. “We expect stable property markets and strong capital availability to continue to support mortgage borrowing and lending in ‘18.”

MBA forecasts mortgage banker originations of just multifamily mortgages at $235 billion this year, with total multifamily lending at $271 billion. After strong growth for ‘17, multifamily lending is expected to slow slightly in ’18, the association said last week.

Also last week, MBA predicted that on the residential side, we’ll see $1.2 trillion in purchase mortgage originations nest year, a 7.3% increase from ‘17. In contrast, MBA anticipates a 28.3% drop in refinance originations next year to approximately $430 billion. In total, mortgage originations will decrease to $1.6 trillion in ‘18 from $1.69 trillion in ‘17. For 2019, MBA is forecasting total originations to rebound to $1.64 trillion, with purchase originations of $1.24 trillion and refinance originations of $395 billion.

MBA chief economist Michael Frantatoni says the association predicts home purchase originations will increase at “a faster clip” in ‘18, nearly double the rate that they increased this year. “The housing market has been hamstrung by insufficient supply, with inventories of homes remarkably low given the home price growth we have experienced.

“The job market remains strong, demographic trends are quite favorable, mortgage credit is becoming more available to qualified borrowers, and home prices should continue to rise,” he continues. “All the pieces are in place for stronger growth in ‘18 and beyond.

Frantatoni says MBA anticipates overall economic growth at 2.0% in ’18,after which it will slow slightly to 1.9% the following year and 1.8% in 2020. “We still expect long run growth potential in the US to be somewhat lower, as productivity gains have been persistently slow,” he says.

“Although inflation remains low, a tight job market is likely to increase inflationary pressures in the near term,” says Frantatoni. MBA expects the Federal Reserve to raise short-term borrowing rates again in December, three times next year and twice in ’19.

“The Fed has begun reducing the its holdings of Treasury securities and mortgage backed securities, and this will put additional, modest upward pressure on mortgage rates,” he says. “We expect that the 10-year Treasury rate will stay below three percent through the end of 2018, and 30-year mortgage rates will stay below 5%.” He adds that MBA expects monthly job growth of 125,000 for ’18, down from the monthly average of 150,000 seen this year, and that the unemployment rate is expected to drop to 4.0% by the end of next year.

By: Paul Bubny (GlobeSt)

Click here to view source article.

Archives for October 2017

Fall 2017: Harvesting Success Gathering Past Lessons Preparing for the Future

Download the brand-new issue for a 4th quarter commercial real estate economic outlook, key legislative issues for the winter, negotiation techniques from CCIM, and more. Plus – enjoy a look into the future with CRE®’s Top 10 Trends.

This Fall 2017 issue contains an update from President Brown, an economic outlook for this year’s 4th quarter of commercial real estate, key issues for the winter, negotiation techniques, international business, networking, and more.

Download the Issue

By: National Association of REALTORS®

Click here to view source article.

The CRE® Top Ten Issues Affecting Real Estate 2017-2018

Global uncertainty and political polarization top the list of issues expected to have the most significant impact on real estate throughout 2017- 2018, according to The Counselors of Real Estate ®, the invitation-only professional association for the industry’s leading real estate advisors. The Counselors’ 1,100 global members undertake extensive collaborative dialogue on issues and trends to finalize the annual list.

1. Political Polarization and Global Uncertainty

Political Polarization and Global Uncertainty are impacting decision-making at every level of government and the business community. Recent elections in the U.S. and other countries point to resurging nationalism and test relationships around the globe. Potential military conflicts seem more likely. Negative implications on real estate are immediate. Uncertainty about trade, travel and immigration threaten cross-border investing, infrastructure, affordable housing, local and state pension liabilities, and education.

2. The Technology Boom

Technology is revolutionizing real estate as it changes the way real estate is bought, sold, and managed. Commercial real estate tech start-ups have grown exponentially over the past 5 years. Robotic learning has accelerated automation in the workplace; as many as 47% of today’s jobs could be replaced by automation. Big Data supports real estate planning, investment, and space planning decisions. Online consumption drives warehouse demand up and retail space down.

3. Generational Disruption

Boomers’ and Millennials’ divergent views of where to live, work, and play impact the property markets. The generations cross paths everywhere and share space, despite disparate demands on the built environment. Real estate professionals need to understand not only the location preferences of each generation, but the design and amenity features, whether rental or owner occupied. One size will not fit all.

4. Retail Disruption

We are not, by any stretch, facing a “Retail Apocalypse.” Restaurants are booming. Grocery-anchored malls remain steady. The trend toward transforming retail into “experiences” continues to drive customer traffic to an environment targeted to a variety of age groups and interests. “Omni Channel” platforms encompass e-commerce and a host of spaces, physical and virtual. And, as retailers refine inventories, distribution methods, and fulfillment models, the retail market will survive– even prosper – in fresh, new ways.

5. Infrastructure Investment

The movement of goods is strained, aging, and highly vulnerable. In all forms (roads, bridges, pipelines, etc.) infrastructure needs have become more pronounced. Trump administration proposals suggest limited Federal Government investment, placing heavy reliance on local and state governments and public-private enterprises. This presents important opportunities for the private sector to direct significant funds to infrastructure projects, recognizing the need for infrastructure investment.

6. Housing: The Big Mismatch

A confounding supply-demand mismatch continues to impact markets worldwide. Lack of inventory has generated price spikes, fueling a growing affordability gap, particularly in coastal regions, where highly paid workers monopolize new, resale, and rental product, raising prices on once-affordable housing — creating a crisis for lower paid workers. Insufficient investment in, and government limitations on, creative housing solutions could lead to an affordability crisis.

7. Lost Decades of the Middle Class

Middle class incomes hover below inflation-adjusted levels from almost two decades ago. Middle class jobs remain under pressure, and disenchantment has influenced the rise of populist candidates in many countries. Middle market retail properties bear the brunt of store closures. Rising costs and debt are delaying home purchase decisions. Rentals do not necessarily benefit in the most expensive urban locations, where supply in multifamily housing lags demand, pushing rents higher.

8. Real Estate’s Emerging Role in Health Care

The real estate industry has emerged as a major player in improving health. Medical services are delivered in clinics, urgent care facilities, and ambulatory surgery centers, reducing hospital visits. In addition, beyond care facilities, building occupants increasingly demand that the space they occupy be designed, constructed, and operated in ways that improve health outcomes. Buildings designed to address health behaviors (i.e., the WELL Building Standard) are a growing trend.

9. Immigration

More restrictive immigration laws appeal to voters concerned about jobs and security. At the same time, many companies bemoan the lack of qualified workers. Development projects stall from labor shortages. New immigrants also tend to rent, boosting demand for multifamily housing, and they aspire to own homes. Labor mobility and homeownership are constrained by limiting immigration, and economic growth is curtailed, with a smaller labor force to support an aging population.

10. Climate Change

The National Oceanic and Atmospheric Administration (NOAA) released a new report doubling forecasts of potential sea level rise by 2100. Most coastal areas are exposed to risk, while Miami, New York, New Orleans, Tampa, and Boston are projected to have the greatest problems. Commercial properties in coastal regions will suffer if tenants go elsewhere. Residential properties are vulnerable, with those counting on the equity from their home likely to sell before value declines.

By: Peter C. Burley (NAR)

Click here to view source article.

Commercial Real Estate Displays Signs of a Maturing Cycle

What an eventful year 2017 has been! We weathered winter snowstorms, summer record heat, strong hurricanes and 500-year floods. We watched as campaign promises have gotten mired in legislative tall grass. We cheered as consumers found more jobs and higher wages, only to see those wages outpaced by steeper housing costs. We listened intently as the Federal Reserve announced its plan to unwind its monetary easing by shrinking the assets on its balance sheets. We watched as equity markets met these and other events with optimism by hitting new highs. And the year is not over yet.

Commercial Investments Remain Bifurcated

For commercial real estate, the year witnessed evolving fundamentals. Demand for space remained solid across the core property types, leading to continued declines in vacancies. Even as new supply picked up the pace, rent growth advanced. However, markets are displaying signs of a maturing real estate cycle.

Despite rising cash flows, investors have taken a significantly more cautious approach to commercial acquisitions. On one hand, with the Fed tapering its quantitative easing, investors expect interest rates to rise over the medium term. On the other hand, the gap between what sellers expect to receive and what buyers are willing to pay has grown wider.

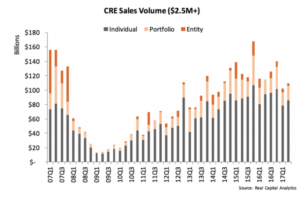

Investment sales in large cap markets declined in the first half of 2017 (H1.2017). The volume of commercial sales at the upper end totaled $211.1 billion in H1.2017, a 9.3 percent year-over-year decline, according to Real Capital Analytics (RCA). The yearly investment volume declines were sharper for portfolio and entity transactions, which declined 12.5 percent and 55.1 percent, respectively. Individual transactions slid by 6.3 percent from the first half of 2016. Mirroring underlying shifts in market trends, sales of apartment and retail properties posted double-digit declines during the first six months, while office transactions inched down a slight two percent. Riding favorable trade activity and robust e-commerce demand, industrial properties proved highly attractive for investors, with sales posting a 10.0 percent year-over-year gain.

In contrast to the sales declines in large cap markets, commercial real estate investment in small cap markets–where a majority of REALTORS® is active–regained its upward momentum by the midpoint of the year. Sales volume in REALTOR® markets returned to an upward trend after the first quarter’s slide, advancing 4.4 percent in the second quarter, based on data from the National Association of REALTORS®. In addition, a larger percentage of REALTORS® reported closing transactions–75.4 percent, compared with 61.0 percent in the first quarter–a sign of growing activity.

Pricing Flattens

While investment trends bifurcated along deal values, pricing trends moved in concert in both large and small cap markets during the first half of the year. Cap rates have been at historic low levels, with those in markets tracked by RCA averaging 6.9 percent during the period. Cap rates in large cap markets have flattened over the past few months, and are unlikely to contract further given the tightening monetary policy. Pricing data from RCA’s Commercial Property Price Index registered a 6.0 percent gain in the first six months, with most of that driven by advances in office and apartment properties.

Other commercial real estate price indices offered similar trends. The Green Street Advisors Commercial Property Price Index–focused on large cap properties–was flat, with a 0.1 percent gain on a yearly basis during the second quarter, at a value of 125.8. The National Council of Real Estate Investment Fiduciaries (NCREIF) Price Index increased 6.3 percent year-over-year in the same period, to a value of 270.7.

In small cap commercial markets, REALTORS® reported that the shortage of available inventory remained the number one concern, and counted as the main driver of price movement. Prices for commercial properties increased 6.7 percent by the midpoint of the year compared with the second quarter of 2016. However, capitalization rates changes mirrored broader trends, rising 30 basis points to an average of 7.3 percent in the second quarter of the year. Not surprisingly, due to the tight inventory, the gap in pricing between buyers and sellers weighed on REALTORS®’ markets, ranking at number two of top concerns.

Outlook

As the economic underpinnings advance at a moderate pace, commercial fundamentals are expected to maintain an upward trajectory. With employment in business and professional services still driving growth, demand for offices should remain solid. The industrial sector continues to ride the tail winds of trade and e-commerce. Even as store closures have dampened the outlook for the retail sector, demand for space is likely to continue, driven by consumer spending and changing shopping patterns. Multifamily properties benefit from a double-dose of boost–rising household formation and a shortage of residential housing–which will keep vacancies in check, even with rising new supply.

On the investment side, the slowdown in sales volume in large cap markets during the past year and a half points to stabilization and a maturing of the current cycle. Price growth in large cap markets is slowing down and likely to flatten over the coming months. While small cap market lag their larger counterparts by about three years, the general trends are likely to trickle down over the medium term.

By: George Ratiu (NAR)

Click here to view source article.