Slower growth—but how slow? A recession isn’t in the cards as long as the trade war with China doesn’t escalate.

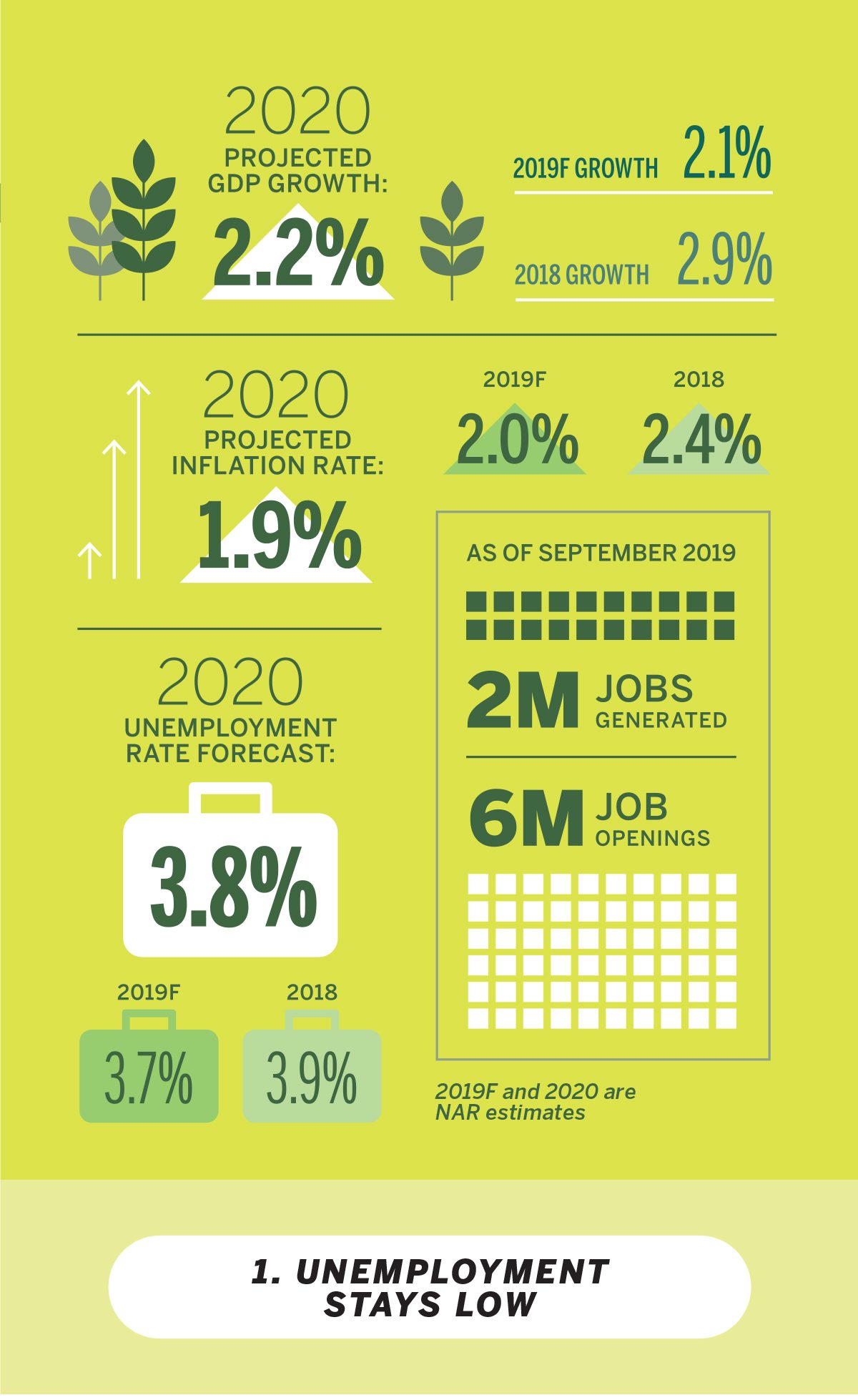

It’s hard to avoid recession chatter these days. Fueling such talk has been a slowdown in the pace of the economic growth in 2019 and the widespread expectation that the long-running economic expansion, which began in June 2009, is nearing its end. The economy is expected to grow modestly—by 2.2%—in 2020, barely higher than the projected growth of 2.1% in 2019, and much slower than the 2.9% expansion in 2018, when the economy got an initial boost from the federal Tax Cuts and Jobs Act.

Still, National Association of REALTORS® Chief Economist Lawrence Yun says a recession is unlikely in the year ahead. “We expect 2020 will be a year of slower growth but not a recession year. However, an all-out trade war would lead to an economic downturn in nearly every country, including the U.S.,” he says.

1. Unemployment Stays Low

The negative effects of the U.S.-China tariff fight include contracting exports and slumps in investor confidence and business spending. But overall, the economy has managed to grow on the back of strong consumer spending, generating about 2 million new jobs in 2019, with real wages rising. Unemployment reached a low of 3.5% in September, and job openings exceeded the ranks of the 5.8 million unemployed workers. The unemployment outlook remains steady at 3.8%.

2. Mortgage rates to sustain housing demand

“We don’t foresee the Fed raising the federal funds rates in 2020. A rate cut of at least 25 basis points in early 2020 is the likely scenario,” says Yun. With the Fed maintaining a low-interest-rate policy, the 30-year fixed mortgage rate is expected to average 3.8% this year. Rates for 15-year fixed mortgages are also trending downward, from 3.4% to 3.1%. Low mortgage rates make purchasing a home more affordable, especially among the 46.5 million 25- to 34-year-olds who made up last year’s largest segment of home buyers. Given the existing conditions, home sales—existing and new homes combined—are expected to increase by a little over 4%, from 6 million in 2019 to 6.3 million in 2020.

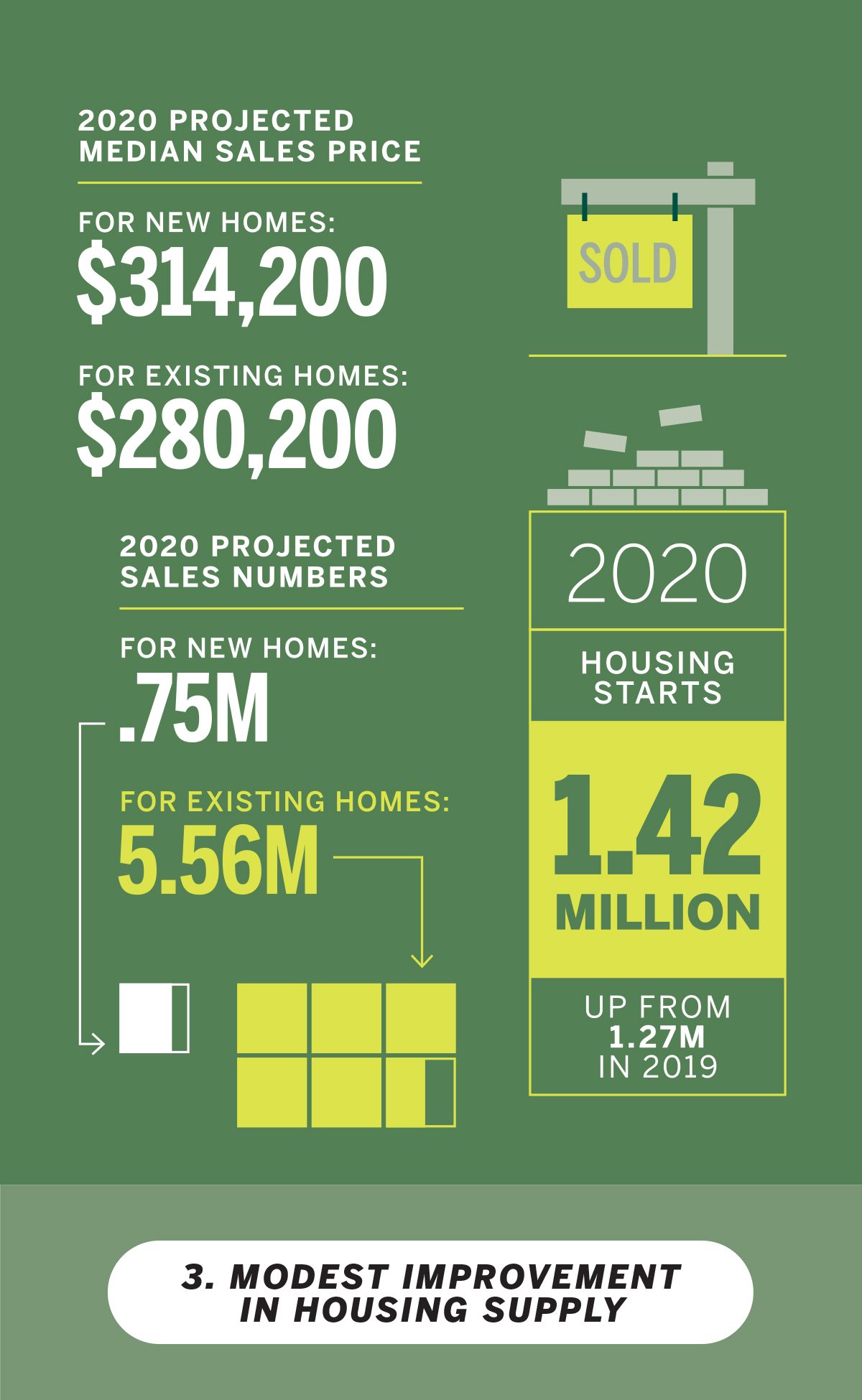

3. Modest improvement in housing supply

Lack of housing inventory has been the primary constraint on the housing market. The housing supply is expected to improve this year, with housing starts expected to hit 1.42 million, up from 1.27 million last year. Still, the new supply will not meet the demand that will be created in 2020 by new household formation, estimated at 1.2 million, and demolished or obsolete housing, estimated at about 450,000. “Ramping up housing construction will continue to be central to improving home affordability and raising the level of home ownership,” says Yun.

4. Commercial

Bright Outlook for Multifamily and Industrial Properties

In the commercial market space, investors are expected to pay a premium for multifamily, industrial, and warehouse properties because of low rental vacancy rates and the sustained demand for ecommerce sales. Cap rates for these properties will likely remain historically low due to the premium for these properties over other assets like offices and retail malls.

Industrial properties are expected to continue to offer good returns for investors given the sustained demand for industrial space from online and traditional brick-and-mortar stores. Both are fiercely competing for consumer loyalty and spending by offering both offline and online shopping options. Examples include Amazon buying Whole Foods, Walmart offering delivery services, quick consumer gratification through one-day or same-day delivery from Amazon and other retailers, and experiential shopping, such as yoga clothing retailer Lululemon offering yoga classes.

The multifamily rental market, including owner-occupied housing, has suffered from inadequate construction. Low rental vacancy rates mean higher demand for apartments and high net operating income for investors. Investments in the multifamily market are needed to address the serious affordability problems for renters. “More multifamily construction, especially of affordable types such as microapartments in San Francisco and more affordable garden-type apartments elsewhere, will help ease the burden for renters,” says Yun.

Affordable Multifamily Housing Strategies

Nationally, nearly half of renters pay 30% or more of their income on rent and utilities. But in 10 states, the percentage of households spending 30% or more on rent is even higher: Florida (56.5%), Louisiana (55.8%), California (54.6%), Hawaii (52.9%), Delaware (52.6%), Connecticut (52.5%), New York (52%), Colorado (51.3%), Nevada (51.1%), and New Jersey (50.9%). Rising rents have spurred California, Oregon, and New York to pass statewide rent-control measures, but rent control is not a sustainable solution to a problem that is borne of a housing shortage. Rising rents can best be addressed by measures that increase the supply of affordable housing:

• Allowing more density in single-family zoned areas (such as in Minneapolis and Oregon);

• Permitting higher-density housing near transportation hubs (Minneapolis);

• Establishing inclusionary zoning policies, especially in opportunity zones that are financially viable for commercial developers and investors (Washington, D.C.);

• Reducing approval time and the uncertainty for project approvals and the associated cost arising from construction delays (such as easing utility and parking regulations for accessory dwelling units in California).

By: Gay Coroaton (REALTOR Magazine)

Click here to view source article