From Brooklyn to Minneapolis, turning are turning empty hotel suites into private dining rooms for small groups.

Faced with a winter full of indoor and outdoor dining shutdowns, chefs across the country have discovered a new place to feed customers: hotel rooms that stand empty during the pandemic.

From Brooklyn, N.Y., to Minneapolis, restaurants are turning suites into private dining rooms for small groups. This comes at a time when the country’s hotel occupancy rates remain at historic lows—65% are below 50 % occupancy—and the restaurant industry faces continued job and revenue loss.

Philadelphia’s Walnut Street Cafe has created individual dining experiences in the AKA University City hotel, located 23 floors above the restaurant in the same mixed-use space. The three-course dinner at what is dubbed “Walnut Suite Cafe”goes for $65, plus a $50 room charge to keep the space for three hours, and is available in 15 of the AKA’s one- and two-bedroom suites. The restaurant’s co-owner, Branden McRill, started the program after the city shut down indoor dining in late November.

“We had so few options for serving guests, so I said, ‘Let’s try this,’” he says. Guests are required to follow Covid-related precautions, such as wearing face covering on entering the property and going directly up to the room.

AKA’s suites are already outfitted with dining room tables, so they easily transition to a private restaurant space. Guests choose from options such as braised beef cheeks and vegetable cannelloni. They can also elect to stay overnight and use the $50 fee toward a room credit. (Suites start at $275.) Otherwise the fee covers AKA’s cost of cleaning the room. McRill says the outlay has been modest; the restaurant has spent about $2,000 to create specially designed carts and hot boxes to bring the food from the kitchen up to the dining rooms. But the arrangement has allowed the restaurant to serve some 60 customers a night, about the same number as indoors before the pandemic.

McRill plans to keep the program into 2021, depending on demand and room availability. Walnut Street Café shares the same ownership company, Brandywine Realty Trust, as AKA University City, which eased the collaboration, according to the hotel’s managing director, Evan O’Donnell. “We wanted to make it an attractive enough price point that it wouldn’t scare people away; we’re not trying for $350 a meal here,” he says.

Le Crocodile in Williamsburg, Brooklyn, was early to adapt the model. In late October, Le Crocodile Upstairs opened in 13 rooms on the 2nd floor of the Wythe hotel. The extension of the popular French restaurant offers a $100 three-course menu for parties of four to 10 people. Options, such as roast chicken with frites and pork steak with chanterelles, are also available on the restaurant’s full menu.

“There’s a lot of demand,” says restaurant owner Jon Neidich. “On the weekends, we’re often fully booked.”

In Minneapolis, the Hewing Hotel has removed beds from several rooms to make way for private dining spaces. And at the Eliot Hotel in Boston, a handful of rooms are being used by in-house dining spot Uni, to serve ramen and sushi, with the restaurant’s music piped in. Other hotels are following suit. The NoMad in New York is offering the “NoMad Feast” in empty suites, featuring such dishes as its signature black truffle-stuffed chicken.

Le Crocodile’s Neidich says customers tend to open their wallets wider in the hotel rooms, because they are viewing the out-of-their-home experience as a special occasion.

“They order more, a nicer bottle of wine,” he says. “The check averages are higher. That means people are enjoying themselves.”

Source: “Restaurants Are Setting Up Shop in Empty Hotel Suites“

Archives for December 2020

Get Ready for 2021 By Reviewing the “Top 10 in 20”

Tune in to the latest episodes of the CRE Thought Leaders Podcast. The “Top 10 in 20” series features brief 20-minute episodes discussing each of the 2020-21 Top Ten Issues Affecting Real Estate, including Economic Renewal, Space Utilization, and Public and Private Indebtedness. Listen online today

Source: “Get Ready for 2021 By Reviewing the “Top 10 in 20”

Every Type of Investor Is Looking into U.S. Industrial Properties

In addition to the usual suspects, ultra-high-net-worth investors and foreign entities are making more industrial bets.

Driven by the pandemic, acceleration in online shopping and an increase in onshoring of manufacturing, demand for industrial space continues to outpace supply in many markets. Over the last couple of months, a significant number of large industrial portfolios and complexes changed hands, as institutional and private investors from both the U.S. and abroad, including equity funds, placed capital in this sector.

“The capital chasing industrial is broad-based, but it’s the usual suspects [who] are active—REITs, pension funds, insurance companies and private equity firms. But global capital is pouring into U.S. industrial as well, including sovereign wealth funds, global financial institutions and pension funds,” says Orange County-Calif.-based Mike Kendall, executive managing director for investment services, Western region, with real estate services firm Colliers International. These investors view this asset class as a “flight to safety,” he notes.

The Lease You Can Do

Understanding the different perspectives of tenants and landlords is key to the lease modification process.

By definition, a market disruption is a situation where a market stops functioning regularly, which usually results in a steep, significant decline. The global COVID-19 pandemic that will define 2020 is a disruption like none other. For commercial real estate professionals, one significant concern is the fundamental relationship between tenants and landlords. As economic instability reverberates across all sectors and in every geographic area, leases will be under strain.

Every morning, you can see headlines that reflect a changing industry. E-commerce has been a bright spot in the national response to COVID-19, with major repercussions for real estate. Landlords across sectors are faced with difficult questions resulting from tenants under stress. Is forbearance a way to keep tenants in properties? Are rent deferrals a short-term solution to disruptions in retail, multifamily, hospitality, and other sectors?

Pinterest offers one huge example of how quickly things can change in the office market. Back in March, literally hours before the coronavirus led to massive shutdowns across the U.S., the online giant signed a deal for 490,000 sf of office space in San Francisco, adding up to $440 million in total payments over the life of the lease. Flash forward to August, Pinterest decided to pay the landlord $89.5 million to cancel the contract. In this case, the tenant calculated the discounted value of the office space and decided to negotiate with the landlord/owner to reach an agreeable settlement – one that totaled 20 percent of the $440 million in payments.

Clearly, things are not what they were just months ago. In light of a tumultuous commercial real estate market, lease modifications will be a hot topic moving forward. To prepare for these negotiations, it’s vital to understand the perspectives of stakeholders so agreements can be made on modifications that satisfy all parties.

Who Are the Stakeholders?

The list of parties in a typical lease isn’t too long — often it’s tenants, landlords, property managers, and lenders. In simple terms, these four are each a leg of a stool, where they rely on one another to remain operational. For a renegotiation to be successful, these players need to work together to preserve an asset’s income and value.

Landlord: Strong revenue, offset by cost recovery and other tax advantages, generate annual income and very positive before- and after-tax yields (IRR). Timing of the cash flows is important to reach the desired yield determined at acquisition. During a disruption, however, both the return and future value of the property can come into jeopardy.

Property Manager: A property manager maintains the property with the goal of achieving the highest annual income (NOI) to the landlord and controlling expenses, all while handling the day-to-day operations of the property and keeping the tenants satisfied. Working with the tenants to ensure their success and communicating difficulties to the other parties or the landlord is paramount during a disruption.

Tenant: Tenants care about the property being maintained throughout the tenancy. Lack of proper care, for example, can reflect negatively on the tenant with customers and employees. Even though the tenant may be in distress and require assistance during a disruption, they are still concerned with the operation and viability of the property. They want to know the landlord will continue to maintain the property and continue to be financially solvent.

Lender: Not all lenders are alike. Depending on the type of loan, they can assist an owner of a property during difficult times or hinder the process due to inflexibility. Commercial mortgage-backed securities, for example, are especially difficult to alter because additional debt isn’t an option. Meanwhile, lenders’ willingness to renegotiate with local/national banks and private institutions varies.

When comparing the goals of tenants and landlords in any renegotiation, you first need to understand the goals of each party. Both want to preserve income and continue to be able to pay all obligations. Tenants, though, are hoping to maintain business income and keep control of the location, while landlords are interested in preserving the value of the building and maintaining ownership of it.

Case Study

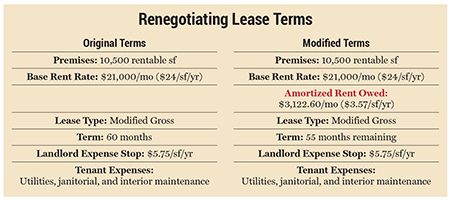

To see how these concepts operate in the field, let’s examine a hypothetical case study. Med Resources Inc. is the tenant in a 10,500-sf office space owned by Equities Plus Inc. Sixty months remain on the term of the lease at $21,000 per month, with the tenant also paying utilities, janitorial costs, and interior maintenance. But since the COVID-19 pandemic, the office has been closed.

Med Resources is facing difficulty, so it approaches Equities Plus to discuss pressing concerns. The landlord wants to assist the tenant through these difficult times, and both parties estimate a time frame of nine months for the continued disruption.

Equities Plus does not need lender approval for the lease modification because the required loan-to-value is still within the covenants of the loan. Med Resources, meanwhile, has agreed to the proposed terms that increases rent from $21,000 per month to $24,122.60 once deferred rent is amortized and included with original base rent.

f you are the broker for Equities Plus, do you recommend your client continue to own the asset through the next renewal or to sell it at the end of Year 3, when rent returns to what it should be in the original lease along with amortized rent, at an 8 percent cap rate?

If the current owners keep the property through the remaining term of the modified lease, they will have a total effective rent of $958,124, with Year 3 net income of $229,096. If they sell at the end of Year 3, the highest possible price would be $2,863,700 (or $229,096 divided by 0.08).

If the landlords offered an 8 percent discount on rent, even though the landlord receives all rents, deferred or not, due to the time value of money, the concessions cost to the landlord is $212,490 over five years in current dollars.

So you have to answer two questions:

- Do I call the additional rent a “loan” to the tenant, which is then credited at face value?

- Do I add the additional rent into the base rent, effectively raising the rent throughout the remaining term (last 46 months) by $3,122.60 per month?

You can see the sale price is $468,000 higher when the amortized deferred rent is added to the base rent because the 8 percent cap rate of the additional rent. The base rent went from $24 per sf to $27.57, with $74,942.40 in remaining rent due at end of third year. When applying a cap rate of 8 percent to the third year NOI of $229,096, the increased property value compared to the original rent amount (NOI) is more than $368,000.

In the end, value was found in later years by modifying the lease and increasing the base rent after providing rent forbearance. In this case, it was a win-win because the tenant received relief while the landlord increased value. Different priorities do not always mean competing priorities.

Looking ahead, as commercial real estate in all sectors works to rebound from the massive market disruption of COVID-19, plenty of questions will need to be answered, including:

- What do future investors need to do when purchasing after a market disruption?

- How does a lease renegotiation impact future options for lease renewals? What if there isn’t a renewal option and the parties want to extend the lease?

- How will lender and tenant approach this conversation?

The new reality in commercial real estate includes some significant obstacles, including mandated closures, operating restrictions, increased customer safety needs, and potentially lower profits given reduced capacities.

We are not in a standard market cycle. But the best CRE professionals will recognize opportunities to assist with lease modifications, and understanding the perspectives of everyone involved is a key first step.

Source: “The Lease You Can Do“